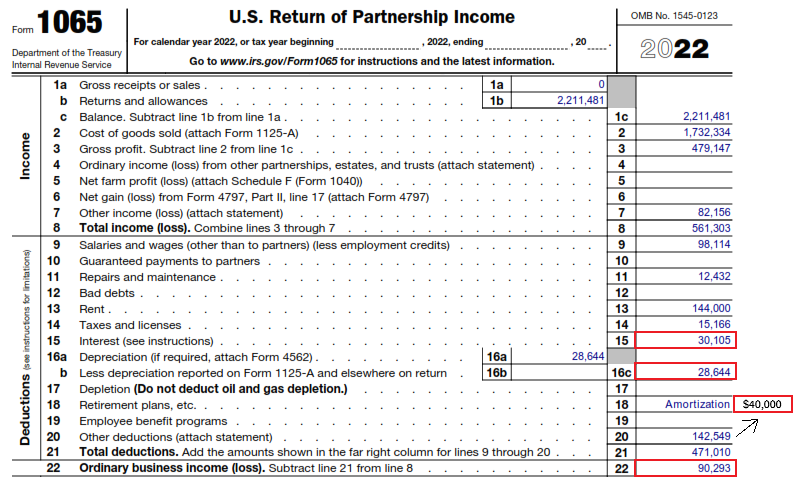

01 May Calculating Cash Flow (Appraiser vs. Lender)

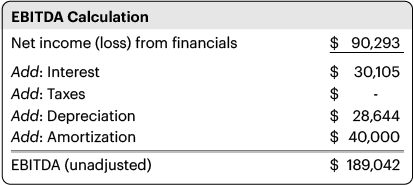

The EBITDA calculation is shown in the table below (this is similar to how a lender calculates EBITDA):

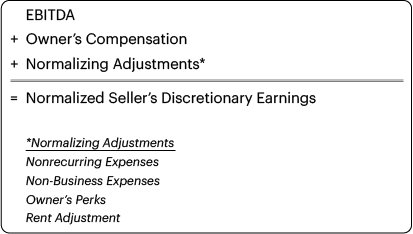

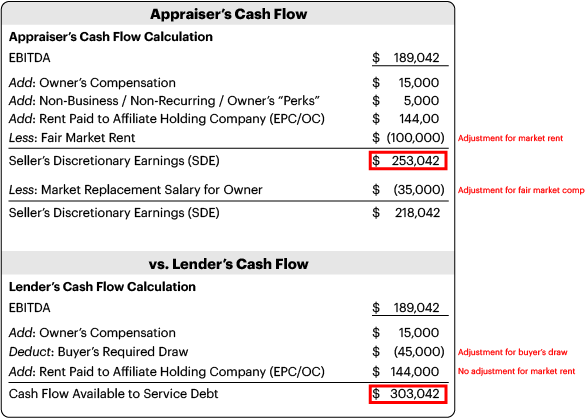

In order to arrive at SDE, the following adjustments are required:

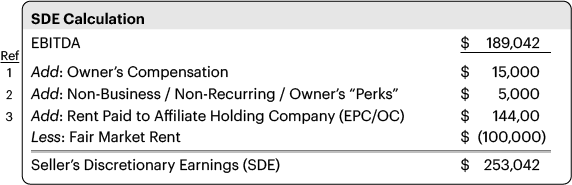

Using the table above, the liquor store’s SDE is calculated in the below:

- Owner’s Compensation is included in the Salaries and Wages expense category (line 9 in the tax return) in this business. When dealing with an LLC (Form 1065) the appraiser must request the owner’s W2 to ensure that this figure is accurate (Guaranteed Payments to Partners is different than a W2 salary). The owner’s compensation in a C Corp (Form 1120S) or S Corp (Form 1120S) is listed under the Compensation of Officers line (line 7 or 12, respectively). It is important to include only the owner’s compensation in this add-back, as there may also be non-owner officers included in this line item. Additionally, if multiple owners work, their salaries must be replaced with fair market replacement salaries, since the SDE earnings stream is for a single owner-operator. Read “Owner’s Responsibilities” article for more information.

- Owner’s Perks include owner’s health insurance premiums paid by the company, included in the Other Deductions expense (line 20 in the tax return). Non-business related expenses (personal auto, owner’s health/life insurance, salary paid to non-working family members, etc.) or nonrecurring expenses (broker’s fee, extraordinary legal fee, etc.) must also be adjusted. Read “Financial Statement Adjustments” article for more information.

- The owner of the liquor store in the example above also owns the real estate under a separate holding company (EPC/OC structure). Anytime there is a non-arm’s length relationship between the business owner and the landlord, a rent adjustment is required, as a hypothetical buyer of the business will be required to pay fair market rent to the landlord. The appraiser must add back all rent paid to the real estate holding company (if any) to the earnings, and then subtract out a fair market rent, which can be based on a real estate appraisal or reasonable estimates of rent per square foot times total square footage. In the table above, fair market rent was estimated at $20/psf multiplied by 5,000 square feet. Read “The Rent Adjustment” article for more information.

Although not shown in the example above, non-operating income must also be removed from the earnings (affiliate company income, interest income, insurance loss reimbursement, gain on sale of fixed asset, etc.).

As seen below, there are some significant differences between the appraiser’s cash flow and lender’s cash flow, namely the rent adjustment and the buyer’s required draw.

Although lenders may determine similar earnings streams as part of their underwriting processes, the adjustments lenders apply to arrive at their earnings streams are usually specific to the deal terms and borrower’s requirements. Moreover, lenders will take into consideration factors such as a specific buyer’s global debt service capability, personal revolving debt, among others – this may require a Buyer’s Required Draw. Meanwhile, cash flows used by business appraisers are determined based on a hypothetical transaction which assumes one owner-operator for the subject business.

SDE is used in the transaction/market approach and is usually applicable for small businesses that are owner operated. EBITDA is used for larger businesses that are commonly absentee owned (operated by a general manager being paid fair market wages). As seen in the table above, the Adjusted EBITDA earnings stream removed the fair market replacement salary for the owner. Because a liquor store is typically owner operated, the EBITDA cash flow stream may not be as relevant in the appraiser’s analysis.

For lenders, the proper calculation of these earnings streams in the context of business appraisals may be of particular importance when applying rules of thumb multiples to determine an initial estimate of value (for instance, to determine the reasonability of a purchase price).

Our next SBAvalue™ article will include a detailed discussion of reasonable valuation multiples that can be applied to the above SDE earnings stream to estimate a final value of any business.