25 May Determining a Reasonable Earnings Valuation Multiple

In the previous SBAvalue™ article Calculating Cash Flow (appraiser vs. lender), we discussed how a business appraiser calculates Seller’s Discretionary Earnings (SDE), which is an integral cash flow stream for small businesses. Once SDE is calculated, the next step is to determine a reasonable multiple (or range of multiples) to apply to the SDE earnings stream. This article will serve as a guide to determine a reasonable and supportable range of earnings multiples for the vast majority of industries financed by SBA lenders. By applying these multiples to the SDE earnings stream, you will have a reasonable range of values for the subject business, often referred to as rule of thumb values.

Our firm’s internal database of business transactions financed by SBA lenders indicates a median multiple for small businesses across all industries to be approximately 3.0x SDE. Based on businesses Reliant has appraised, the general range of SDE multiples across all industries is between 1.5x – 4.0x SDE for small businesses (revenues less than $5 million per year). However, SDE multiples can vary significantly across industries due to a variety of factors, as discussed in the next paragraph.

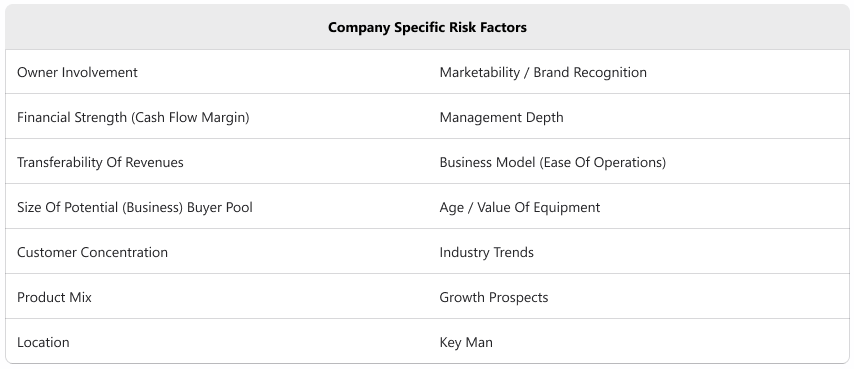

This difference in industry multiples is heavily influenced Company Specific Risk (CSR), which encompasses a set of factors used to compare the subject to its peers, industry, and all other businesses across all industries. The CSR factors include, but are not limited to the following:

Similar to capitalization rates, Company Specific Risk factors have an inverse relationship to the earnings multiple; as the CSR decreases, the earnings multiple increases. Using the table above, let’s continue with the liquor store example from our previous SBAvalue™ article Calculating Cash Flow, and discuss the factors that would influence the multiple for that business:

Liquor Store:

| Owner Involvement | Transferability of Revenues | Size of Potential Buyer Pool | Barriers of Entry | |||

| Low risk – minimal involvement required – only major responsibilities include inventory and personnel management | Low risk – very few customers know (or would care) that a change in management takes place, just as long as their favorite products remain in stock | Low risk – assuming you don’t have any misdemeanors and can own a liquor license, you are qualified as a potential buyer! | Low risk – varies on a state by state basis; if operated in a license quota state, barriers of entry are high as this limits competition from opening up nearby |

Based on the factors above, we can determine the CSR factors of a liquor store are low, as there are minimal ownership involvement requirements, a high transferability of revenues and a significant buyer pool size. Taking these into consideration, a reasonable range of earnings multiples for the liquor store where we calculated SDE to be $250,000 is estimated to be between 3x – 4x SDE, resulting in a value range between $750,000 and $1,000,000. If the subject were operating in a quota state (liquor licenses limited by the town/county), this may warrant a multiple in excess of 4x SDE, depending on the estimated value of the liquor license.

Now let’s take into consideration those same risk factors and apply them to a general dental practice:

Dental Practice:

| Owner Involvement | Transferability of Revenues | Size of Potential Buyer Pool | Barriers of Entry | |||

| High risk – owner is typically the primary practitioner and must be highly involved in the business operations | High risk – potential loss of patients due to a change in ownership/management takes place (many service based businesses have high attrition risk) | High risk – in order to purchase a dental practice, you must be a licensed dentist within the state where the practice is located | High risk – there is nothing from stopping another dentist from opening up a practice nearby |

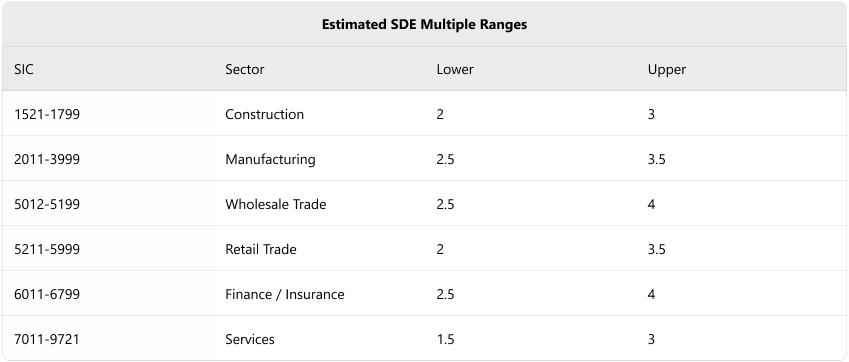

Taking these same factors into consideration above as we did for a liquor store, we can determine the inherent risks of a dental practice. Owners are usually significantly involved in the operations of the business, there is a high risk of attrition due to a change in ownership, the size of the potential buyer pool of the business is limited to only licensed dentists and finally, there are very few barriers of entry for competitors. Based on this, a reasonable earnings multiple for a dental practice should should be 1.5x – 2.0x SDE.The following ranges are reasonable for the most common SIC industry codes:

It is important to keep in mind that not all factors are applicable to each business or industry. For example, a lack of customer concentration should not be seen as a positive factor for retail businesses, as customer concentration is not an inherent risk to the industry as a whole. Meanwhile, location may not be a risk factor for most service-based and manufacturing industries.In order to determine a final earnings multiple, appraisers will analyze the subject on a comprehensive basis, taking into account the subject’s historical financial performance, ratio analysis, quality of financials, how the subject compares to guideline transactions, among many other factors. Although the CSR factors discussed in this article will not provide a means of determining a precise earnings multiple, these factors should help lenders determine a reasonable range of multiples for the subject business being appraised. Ultimately, this should assist the borrower and/or underwriters identify possible valuation issues early in the application process.

It is important to keep in mind that not all factors are applicable to each business or industry. For example, a lack of customer concentration should not be seen as a positive factor for retail businesses, as customer concentration is not an inherent risk to the industry as a whole. Meanwhile, location may not be a risk factor for most service-based and manufacturing industries.In order to determine a final earnings multiple, appraisers will analyze the subject on a comprehensive basis, taking into account the subject’s historical financial performance, ratio analysis, quality of financials, how the subject compares to guideline transactions, among many other factors. Although the CSR factors discussed in this article will not provide a means of determining a precise earnings multiple, these factors should help lenders determine a reasonable range of multiples for the subject business being appraised. Ultimately, this should assist the borrower and/or underwriters identify possible valuation issues early in the application process.