31 Oct The Impact of Intangible Assets on Loan Structure

Prior to obtaining a business appraisal for a change of ownership loan, one of the most important processes for an SBA lender is structuring their use of proceeds and determining the borrower’s equity injection requirement.

As per the SBA’s Standard Operating Procedures (SOP), “If the purchase price of the business includes intangible assets in excess of $500,000, the borrower and/or seller must provide an equity injection of at least 25% of the purchase price of the business for the application to be processed under delegated authority.”

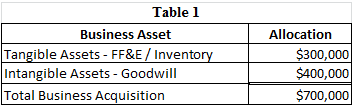

A recurring question we hear from lenders is, “How do I determine the intangible asset value before ordering a business appraisal?” In the absence of a business appraisal, lenders typically base the value of intangible assets on the allocation of sale provided in a purchase agreement. However, this could lead to major issues after the business appraisal is completed, as the allocation is typically determined by the buyer and seller’s accountants, and is primarily based on tax strategies. Based on the allocation in Table 1 below, the lender determined that the borrower’s equity requirement of 10% would be sufficient (to process under delegated authority).

However, intangible assets are specifically defined in the SOP as “…the value of the business as identified in the business appraisal [emphasis added] minus the sum of the working capital assets and the fixed assets being purchased”. Let’s break this definition down:

intangible assets =

business value – (working capital + fixed assets)

Working capital equals Current Assets minus Current Liabilities.

Fixed Assets should be based on one of the following: 1) the net book value as reflected on the most recent balance sheet, or 2) the fair market value as determined in an equipment appraisal.

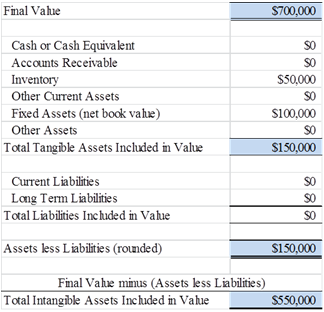

The following table depicts how the final value should be broken out in a business appraisal report compiled for SBA financing purposes. The table shows a structured asset sale which includes fixed assets, goodwill (intangible assets), and inventory.

The fixed asset value is determined using the net book value as reflected on the most recent balance sheet of the business, rather than the allocation of sale as per the purchase agreement. In this scenario, the intangible assets are valued at $550,000 ($700,000 business value – $150,000 working capital and fixed assets), which means a borrower and/or seller must provide an equity injection of at least 25% of the purchase price of the business to process the loan under delegated authority. [It’s important to note, as per the SOP, when calculating the equity requirement dollar amount, the term ‘purchase price of a business’ includes all assets being acquired such as real estate, machinery and equipment, and intangible assets. Inventory should also be factored in if it is included in the purchase.]

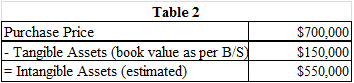

So how does the lender determine the value of intangible assets before an appraisal is engaged, in order to estimate the borrower’s equity injection requirement? As depicted in Table 2, rather than using the allocation of sale, the lender can use the book value of tangible assets as per the most recent balance sheet, and subtract that balance from the proposed purchase price:

If working capital is included in the transaction and purchase price, it should be included under tangible assets (at book value). This way, the intangible asset value is estimated prior to ordering the business appraisal, and the business appraisal can simply verify the amount is correct – if the final value concluded in the business appraisal is different from the purchase price, the lender can make the appropriate adjustments.

Equipment Appraisals

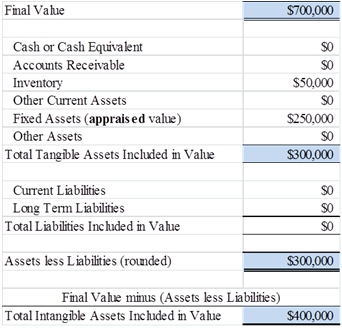

As seen in the table below, replacing the net book value of fixed assets with the fair market value concluded in an equipment appraisal may result in a change to intangible assets. Notice that the final value of the business does not change if the fixed assets are appraised, but the tangible and intangible values shift. The change in the value of intangible assets may impact the borrower’s equity injection requirement – in the table below, the intangible asset value drops from $550,000 to $400,000.

Conclusion

Rather than relying on purchase agreement allocations to estimate intangible asset value, lenders should use the business purchase price and the book value of tangible assets to estimate the intangible asset value. Once a business appraisal is engaged and issued, a cross check can determine if the loan needs to be restructured – but this will typically prevent the lenders from having to ask the borrower to significantly change the equity injection in the 11th hour.