17 Oct Policy Changes in the SBA SOP 50-10 5(J) that Impact Business Valuations and Equipment

The SBA has released an updated version of its Standard Operating Procedures (SOP) 50 10 5(J), which is effective January 1, 2018. The following discussion highlights key revisions in the SOP which affect both business valuations and equipment appraisals, along with the author’s comments.

7(a) Loan Program –Business Valuations Requirements (pg. 196-198)

Terminology

Throughout the new SOP, the term “business appraisal” has reverted to “business valuation”.

Qualified Source

- The ABCA acronym was incorrect – the correct designation is BCA (Business Certified Appraiser), and this has been updated in the new SOP.

- Effective April 1, 2013, the AVA credential has been merged into the CVA, and lenders should recognize the AVA certification is no longer in existence. However, this was not updated in the new SOP and incorrectly remains a “qualified source”.

- Reminder: CPAs are still not considered a “qualified source”, unless they also possess the ABV (Accredited in Business Valuation) designation.

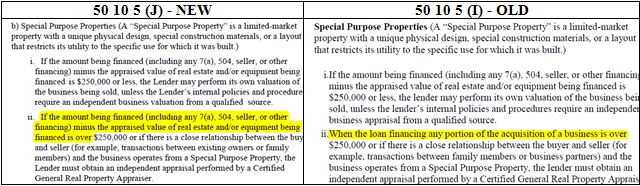

Special Purpose Properties

The highlighted language in paragraph ii below was tightened up as the previous version of the paragraph caused confusion and was likely unintended to be different than paragraph i:

A new list of Special Purpose Properties in on pages 259-260 – the new SOP notes that this list is not all-inclusive. Only six examples are given in the new version:

i. Car wash business;

ii. Gas stations;

iii. Hotels, motels and other lodging facilities;

iv. Hospitals, nursing homes and assisted living centers;

v. Marinas; and

vi. Farms, including livestock and dairy facilities.

The previous SOP 50 10 5(I) provided a more extensive list of Special Purpose Properties (found here), which (in my opinion) should still be referenced when the property type is still in question (also refer to the definition of Special Purpose Property – “a limited-market property with a unique physical design, special construction materials, or a layout that restricts its utility to the specific use for which it was built”).

Transaction Type

The following paragraph was moved up to the top of the Business Valuation Requirements section, most likely due to the importance of its contents. Of particular importance is the sentence highlighted in bold – failure by the lender to confirm the appraiser has followed this guideline could put the lender’s guarantee at risk.

In order for the individual performing the business valuation to identify the scope of work appropriately, the business valuation must be requested by and prepared for the Lender. The scope of work should identify whether the transaction is an asset purchase or stock purchase and be specific enough for the individual performing the business valuation to know what is included in the sale (including any assumed debt) [emphasis added]. The business valuation must include the individual’s opinion of value, the qualifications of the individual performing the appraisal and their signature certifying to the information contained in the appraisal. The Lender may not use a business valuation prepared for the Applicant or the seller. The cost of the appraisal may be passed on to the Applicant.

7(a) Loan Program – Equity Requirements (pg. 174)

Change of Ownership

Minimum equity injection requirements for certain Applicants or loans:

(i) Resulting in a new owner (complete change of ownership): SBA considers an equity injection of at least 10 percent of the total project costs to be necessary for such change of ownership transactions. Seller debt may not be considered as part of the equity injection unless it is on full standby for the life of the SBA loan and it does not exceed half of the required equity injection [emphasis added];

(ii) Change of ownership between existing owners (“partner buyout”): The pro-forma equity position after the change of ownership must be at least 10 percent of the total assets. Otherwise, the remaining owner(s) must provide an additional equity injection that will result in at least a 10 percent net worth (maximum pro forma debt-to-worth ratio of 9:1).

You can still reference the previous SBAvalue™ article regarding equity requirements in a partner buyout, but the 25% will be changed to 10% effective January 1, 2018.

Of importance is the new version of the SOP removed the requirement for 25% equity injection when intangible assets exceed $500,000 in change of ownership loans in order to process under a Lender’s delegated authority. Delegated Lenders may process any change of ownership under their delegated authority, and must comply with the minimum equity requirements as stated above.

7(a) Loan Program – Equipment Appraisals (pg. 186-187)

Collateral Requirements (loans over $350,000)

The acronym FF&E (furniture, fixtures and equipment) should no longer be referenced, as the SBA has intentionally separated machinery and equipment from furniture and fixtures, as highlighted in bold below.

i. New machinery and equipment (excluding furniture and fixtures)[emphasis added] may be valued at 75% of price minus any prior liens for the calculation of “fully-secured”;

ii. Used or existing machinery and equipment (excluding furniture and fixtures)[emphasis added] may be valued at 50% of Net Book Value or 80% with an Orderly Liquidation Appraisal minus any prior liens for the calculation of “fully-secured”;

…

iv. Furniture and Fixtures [emphasis added] may be valued at 10% of Net Book Value or appraised value.

b) If there is a collateral shortfall (not “fully-secured”) on the SBA-guaranteed loan the Lender:

ii. May include trading assets as necessary (using 10% of current book value for the calculation).

Due to this important change, equipment appraisers should now separately allocate aggregate values of machinery/equipment and furniture/fixtures when providing the lender with Fair Market and Orderly Liquidation Values.

504 Loan Program – Collateral Requirements (pg. 312)

Definition of Equipment Appraisals

New language for equipment appraisal requirements utilized in conjunction with the 504 loan program has been added – Of particular importance is the sentence highlighted in bold:

SBA requires that an equipment appraisal be obtained when used equipment is part of the Project and is either being purchased from someone other than an equipment dealer, or being refinanced. The equipment appraisal needs to be a written document from a person that is qualified to provide a valuation, is independent of the transaction, and has performed an onsite inspection of the equipment [emphasis added]. The appraisal must be dated no more than twelve months prior to the date of the application.

‘Project’ as noted above is defined in the SOP as: the purchase or lease, and/or improvement or renovation of long-term fixed assets by a small business, with 504 financing, for use in its business operations.

Although the term ‘qualified’ is not defined, it’s highly recommended that the lender should select an equipment appraiser that provides a USPAP compliant report which defines the lender as the client and intended user and includes the different standard of values (namely, fair market and orderly liquidation values). The appraiser should also possess a reputable appraisal designation, such as one of the following: Certified Machinery and Equipment Appraiser (CMEA), Accredited Senior Appraiser (Machinery) by the ASA or Cerified Equipment Appraiser (CEA) by the AMEA.

Auctioneers, equipment dealers may not be independent of the transaction and therefore should be relied upon. Individuals are not certified or trained in providing USPAP compliant appraisal reports.