17 Feb How Equipment Appraisals Impact Business Valuations

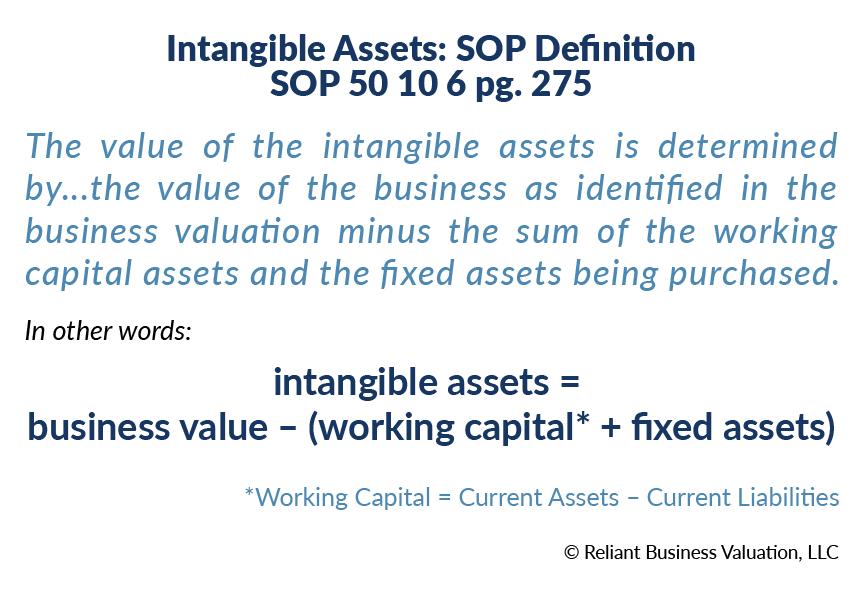

The conclusion of value in any business valuation includes all operating tangible and intangible assets. Tangible assets can include working capital plus fixed assets such as furniture, fixtures and equipment, normally carried on the most recent balance sheet at historical cost less the depreciation (“net book value”). Intangible assets can include goodwill, licenses and customer lists. The combination of these tangible and intangible assets equals the total value of the business. Therefore, the final value includes all operating equipment ‐ adding the appraised equipment value to a business valuation would be double counting the equipment. So how do we separate the intangible and tangible assets?

“Working Capital” is defined as current assets minus current liabilities, calculated by using the most recent book value. In a typical asset sale deal structure, working capital assets would include only current assets (e.g., cash, inventory, A/R, etc.) and no liabilities.

“Fixed Assets” can include furniture, fixtures, equipment and vehicles. The SBA has stated in a prior Information Notice that “If the lender has obtained an appraisal for any real estate or machinery and equipment being acquired, the appraised value may be substituted for the book value for these assets.”

Therefore, a business appraiser must utilize the net book value of the fixed assets when estimating the value of fixed assets, unless a certified third-party equipment appraisal is compiled.

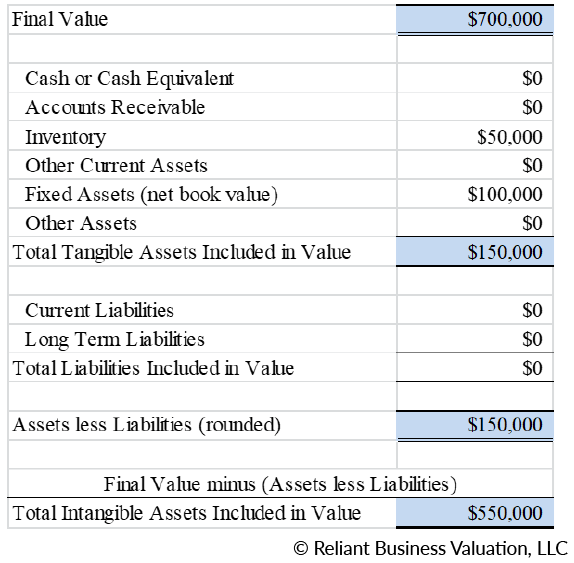

Let’s look at an example: Assume a manufacturing company is appraised at $700,000. It is an asset valuation, and only Inventory (current asset) is included in the purchase price / value (working capital is $50,000). No liabilities are included in the transaction.

Scenario 1: The net book value of the fixed assets is $100,000. In order to estimate the value of intangible assets, the appraiser subtracts the working capital plus the net book value of the fixed assets from the total business value ($700,000 ‐ $50,000 – $100,000), which is $550,000.

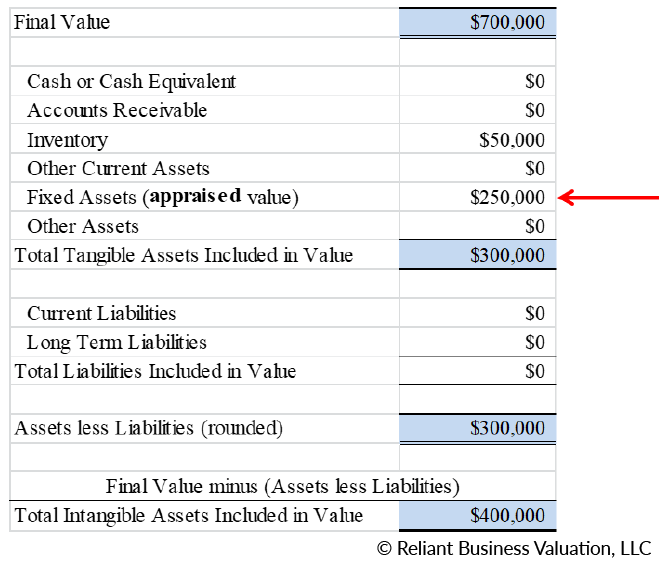

Scenario 2: A third-party certified equipment appraisal was also ordered by the lender. The appraised fair market value of the fixed assets is $250,000. The business appraiser can now use the appraised value of the fixed assets in lieu of the net book value, which effectively decreases the value of intangible assets to $400,000 ($700,000 ‐ $50,000 – $250,000).

Scenario 2 provides the lender with the most accurate value for both tangible and intangible assets, as both assets were appraised separately. More importantly, the lender can use the appraised equipment value in lieu of the net book value, when determining collateral value for their loan.

When ordering an equipment appraisal, the main values to consider as follows:

1. Fair Market Value (FMV):

- No time restriction to sell assets.

- FMV of equipment can be used in Business Valuation in lieu of Net Book Value.

2. Orderly Liquidation Value (OLV):

- Approximately 90-120 days to liquidate and typically 65% of FMV.

- The lender may use 80% of OLV as collateral.

Calculating Collateral

While the Fair Market Value may be used to adjust the goodwill amount in a business valuation, for collateral purposes, the lender must use an Orderly Liquidation Value. The SBA has intentionally separated machinery and equipment from furniture and fixtures. Equipment appraisers should now separately allocate aggregate values of machinery/equipment and furniture/fixtures when providing the lender with Fair Market and Orderly Liquidation Values as follows:

- New machinery and equipment (excluding furniture and fixtures) may be valued at 75% of price minus any prior liens for the calculation of “fully-secured”.

- Used or existing machinery and equipment (excluding furniture and fixtures) may be valued at 50% of Net Book Value or 80% with [sic] an Orderly Liquidation Appraisal minus any prior liens for the calculation of “fully-secured.”

- Furniture and Fixtures may be valued at 10% of Net Book Value or appraised value (OLV).